Success Factors for Wind Power Projects : Gangwon Wind Power

© 2017 by the The Korean Society for New and Renewable Energy

This is an Open Access article distributed under the terms of the Creative Commons Attribution Non-Commercial License (http://creativecommons.org/licenses/by-nc/3.0) which permits unrestricted non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited.

Abstract

Diversification of energy supply became necessary, and as part of efforts to reduce the emission of carbon dioxide, it is imperative to develop environmentally friendly clean energy sources such as wind power energy. The key factors for the success of wind power projects are identified through literature review and the previous studies. Among the various factors, “Feasibility analysis,” “Government tariff system” and “WTG selection,” and “Project Finance” are assumed to be the core factors and the effectiveness is analyzed, by applying to the case of Gangwon wind power (GAWIP). In particular, “Project Finance” is assessed to seriously affect the debt serviceability and the profitability of the project throughout its operating period due to its nature of volatility. This paper presents key risks and success factors of wind power projects and suggests mitigating measures against the risk of financial fluctuations.

Keywords:

Wind Power Project, Success Factors, Feed-in-Tariff, Gangwon Wind Power Project, Project Finance1. Introduction

Recently, as the importance of renewable energy such as oil price instability and UNFCCC (The United Nations Framework Convention on Climate Change) has been recognized again, diversification of energy supply method became necessary. As part of efforts to reduce the emission of coal-fired power plants, which produce carbon dioxide and greenhouse gasses causing global warming, it is imperative to develop and disseminate environmentally friendly clean energy.

Renewable energy is a sort of alternative energy that can be used for pollution-free renewable energy such as solar energy, solar power, wind power, geothermal energy, etc. It is effective to reduce greenhouse gas emissions by replacing fossil fuel,

Among them, wind power has the advantage of a relatively low generation cost among renewable energy sources which are permanent and pollution free, and researches and developments are thus being actively carried out worldwide. Wind power refers to converting wind energy into mechanical energy using a device such as a wind turbine and turning it back to produce electricity using this energy. Wind turbines can theoretically convert up to 59.3% of the wind energy into electrical energy, but in reality, there is a loss factor due to blade shape, mechanical friction, and generator efficiency, so the practical efficiency remains at 20-40%. Nonetheless, benefits of wind energy include climate change and reduction of environmental pollutants, employment promotion and growth of local economies, diversification of energy supply system and substitution of energy import, reduction of disputes between countries/territories for securing energy security and acquiring natural resources.

This wind energy is considered to have a very large potential, and it is analyzed that the economics and development of the technology of wind energy are the most outstanding among the renewable energy sources. In recent years, it shows the possibility of securing competitiveness enough to compete with existing power generation sources. In fact, the area used for the wind farm occupies only 1% of the total area of the entire complex including the foundation of the wind power towers, the road, and the central control room, while the remaining 99% of the area is available for other uses such as livestock and agriculture.1) Also, Wind power is a type of renewable energy that is abundant in resources, constantly recycled, distributed over a wide area, clean, and a promising replacement for fossil energy depletion in the absence of greenhouse gas emissions during operation.2)

For these reasons, wind power has become one of the world's fastest-growing sectors in the energy industry. As a result, the installed capacity of the world has increased six times over the past ten years (486,749MW at the end of 2016). Unit generation price has been continuously lowered with the economy of bigger scale and complex.

In Korea, the development of 2 kW small wind turbines was started in 1975, and the “Alternative Energy Development Promotion Act” was enacted in December 1987 to establish a regulatory basis for the expansion and diffusion of new and renewable energy. In 2002, as part of a policy to expand stable and renewable energy, the FIT (Feed-In-Tariff) was introduced to support renewable energy generation cost and SMP (System Marginal Price). It contributed to the expansion of the initial renewable energy supply through stable profit guarantee of the project, but as the financial burden of the government has increased rapidly, the necessity of new measures has been continuously raised. As a consequence, the government decided to transfer the system to the Renewable Portfolio System (RPS), which is being implemented in the United States and globally. The FIT system in operation for ten years has thus become a new renewable energy supply mechanism for domestic renewable energy supply and industry development. Thanks to the government's continuous support policies and various financial benefits, local governments and power generation companies are competing in the wind power industry.

This study intends to elucidate characteristics of wind power generation business and derives major factors for an efficient and successful operation of wind power projects. For this purpose, we will firstly identify the key success factors and find their theoretical bases through previous studies and literature review, and second, verify them with the analysis of the case of Gangwon Wind Power project (GAWIP). Third, we will examine the implications of the findings and the application of the factors under the RPS system.

2. Literature Review and Theoretical Background

2.1 Process of developing wind projects

In general, as with any other power generation projects, wind power projects will begin with a feasibility study. After analyzing the site's wind resource and selecting a proper WTG model, it will estimate the cost of the project, which is the key concern of investors. A series of these preliminary preparations usually takes 2-3 years, depending on the complexity and it will be typically operated for 20-30 years after a 2-3 year construction period. The Figure below (Deloitte, 2014) illustrates this process well.

Process of development

The development phase features setting up a project layout based on environmental, geological and wind study, for example. Turbines should be deployed such that soil and wind conditions favor lower capex but higher energy production. In addition, a preliminary financial model is established to assess whether the investment cases are economically feasible. Often financial advisers are appointed at the initial investment stage to evaluate their investment cases and introduce their experience and expertise to increase the likelihood of successful project launches.

During the next phase of maturation, in parallel with completion of permissions from the competent authorities, wind power plant designs are refined to ensure optimal placement of wind facilities. Procurement contracts for construction elements and WTG service are conditioned on the construction start. New insights on energy production, tariffs, capex and opex are integrated into fixing the financial model which in turn supports consents from investors and lenders. After FID (Final Investment Decision), the project goes into the final stages of the project lifecycle, which includes construction and afterward operation.

2.2 Literature review

It is hard to find one global common package of success factors for the development and operation of wind power generation. There have been numerous researches on key drivers of the wind projects, but most of them are related to regulatory frameworks as they are very much dependent on the government supports3). For example, in an institutionally immature country, firm establishment of regulations and related technology development are analyzed as core drivers. Meanwhile, in the energy-advanced countries such as the United States, more commercial parameters like wind resource, electricity transmission, policy environment, ownership, and visibility are often cited as major factors to influence the success of the wind power (Blanco, 2009).

As a theoretical ground for our purpose, we intend to refer to a recent study (Lyou et al., 2012) analyzing the key success factors of the wind power plant projects applicable in Korea. In the study, the focus group interview (FGI) was conducted for the wind power industry related experts to identify and determine the key success factors4). Based on the 25 factors identified from the interviews and literature review, the appropriateness of those factors was assessed and analyzed under two criteria of importance and performance.

The results are comprehensively illustrated in the quadrant as shown in Figure 2: the Y-axis represents the degree of importance of certain factors to the success of the wind power project, and the X axis can be interpreted to mean the current level where the factor is managed in the actual project.

Quadrant Map of Key Success Factors

Regarding the importance of core factors, “Wind Resource Survey (B2)”, “Feasibility Analysis (B1)”, “Market Research (A1)”, and “Power Plant Design (D1) are positioned in the Quadrant 1.It means those factors are well recognized in terms of the importance and well managed for performance in the market. In the meantime, the factors such as “Project Finance (A5)”, “A/S material procurement (F3)”, “Operation comparison (F4)”, “Government Tariff System (B3)”, and “Project evaluation at completion (E4)”, scattered in the Q2, are weak and poorly managed in the category of the performance, though having the moderate importance. Lyou (2012) identified and concluded four factors, among 25 factors, based on the score of difference between the importance and the performance, which implies the bigger, the more need improvement for the success5). Those four factors are “Project Finance (A5,2.22)”, “Feasibility analysis (B1,2.20)”, “Government tariff system (B3,1.89)” and “WTG selection (E1,1.78)”.

2.3 Key success factors

If the four factors, jointly or severally, fail to achieve a certain set of conditions or functions, it hampers the successful operation of a project and jeopardizes the project. It needs, therefore, proper and efficient management. Among the factors, “Feasibility Analysis (B1)” and “WTG Selection (E1)” have the nature of endogenous variables manageable by the sponsors of a project, while “Project Finance (A5)”, and “Government tariff system (B3)” are relatively exogenous, beyond the control of the project company. In other categorization, B1, E1, and B3 are more “a priori” as those should be clarified prior to finalization of investment decisions, while A5 would be subject to the satisfaction of the three factors.

“Project Finance (PF)” is thus often more important in executing and maintaining the success of the project. It is very rare in reality for the project sponsors to carry out the project solely with their own funds because external financing is fundamentally necessary to improve the profitability of the project and maximize the investor’s return, i.e. IRR (Internal Rate of Return). In most cases, the funds needed for the project are financed by borrowing from financial institutions in the form of Project Finance.

Looking more closely at the financing, Project Finance represents all financial means for a project in a broad sense, but here it refers to a type of financial technique based on future cash flows as a major reimbursement source. In such, a PF is not based on the credit or conventional assets of the project sponsors but based mainly on the projected cash flow that the project will generate in the future. Therefore, the bankability through project risk analysis and appropriate mitigation is an essential basis for lending decisions. In general, PF lenders have a conservative stance on risk and have the attitude of not accepting risks that are not adequately preassessable because they are likely to generate unexpected risks, or potentially unpredictable risks is. In this sense, the availability of PF can be attributed to the adequacy of risk analysis and mitigation measures to ensure the feasibility of financial support.

This paper intends to confirm the effectiveness of the results of previous studies by applying them to an actual case of a wind power project and to draw some implications.

3. Case Study: Gangwon Wind Power

3.1 Summary of GAWIP

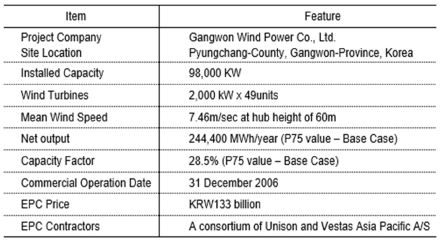

The Gangwon Wind Power Project (Project, GAWIP), summarized in the table below, is a 98 MW wind power project, located in Pyungchang-County, Gangwon-Province, Korea, and was initiated by Unison Co., Ltd. (Unison), a KOSDAQ listed manufacturing company involved in the production of bridge support products, power generation related products and noise suppression equipment, who has been at the forefront of the development of the wind industry in Korea.

Snapshot of GAWIP

Originally the project company had the shareholding structure as shown below, comprising various investors led by Unison taking the role of EPC contractor as well, along with Korea Midland Power Co., Ltd., Military Mutual Aid Association, provincial and municipal governments, Marubeni, Eurus and Lahmeyer International (LI).6) LI also provided engineering and project management services to the Project on the sponsors’ side.

Project structure

The EPC contract has been signed between an EPC consortium comprising Unison and Vestas Asia Pacific A/S (EPC Contractors) on a joint and several basis, on the one hand, and Gangwon Wind Power Co., Ltd. on the other hand. The plant was operated by Unison with a back to back operation and maintenance arrangement with Vestas for the first five years of operation, and after that by itself. Energy generated has been sold to the Korean Power Exchange Market, based on a subsidized price. KRW 107.66 per kWh was set for a period of 15 years post initial completion. The KPX is compensating for the difference between the pool price and the said fixed price undertaken by the government.

The decision to develop the Project was supported by data from various stations of Korean Institute of Energy Research, GAWIP and four existing Gangwon Province’s wind turbines located in the center of the GAWIP’s wind farm site. The wind data obtained was also reviewed by PB Power, the lenders’ technical and wind source advisor. It showed the Project could support the envisaged debt as demonstrated by an average debt service coverage ratio (DSCR) of 1.83x (min 1.39x) on a conservative P75 basis, being the Base Case. On the P90 basis, the average and the minimum DSCRs are 1.77x and 1.33x, respectively.

3.2 Location and wind resource

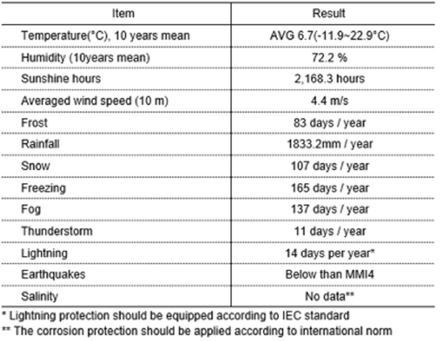

The wind park site is located in the easterly part of the district Pyeongchang in the Gangwon-Province, approximately 9 km north of the city Hoenggye, 35 km inland from the eastern coast. The average elevation of the wind park area is 1,100 meters. Vegetation in the area is principally grass and is extensively free of the forest. A further advantage of the wind park site is the orientation of the ridges transversal to the two main wind directions southwest and northeast, which can optimally boost airflow and allow the wind turbines to be lined up without mutual shading. Because of the location, the site has long winter and has heavy snowfall yearly. The yearly mean temperature in the Taegwallyeong area is 6.7°C. The coldest temperatures usually occur in January with monthly averages from -8 to -6°C. The annual number of days with snowfall amounts to 107 days and the number of freezing days is reported with 165 days yearly (both 10-year averages). The annual precipitation amounts to 1,833 mm. However, the Korean peninsula is monsoonal, and there is great variation in the amount of rainfall over the seasons.

Summary of environmental conditions

The following table gives the general climatic conditions for ten years (1992~2001) in Taegwallyeong close to the wind park site, provided by Korean Meteorological Administration.

On top of wind resource survey conducted by LI, PB Power, the lenders’ technical and wind source advisor, has carried out an independent wind resource and energy production assessment for the GAWIP. There are four monitoring towers located on the site of the proposed wind farm. PB Power considers the wind monitoring equipment and recorded datasets to be acceptable. The data collected from each of the monitoring towers was cross-correlated with 10-year long-term wind speed data from four surrounding reference sites of Taegwallyong, Military Radar Station, Chin Bu, and upper air data from Pohang Station, as well as the actual production data from the four existing Gangwon Province’s wind turbines located in the centre of the GAWIP’s wind farm site.

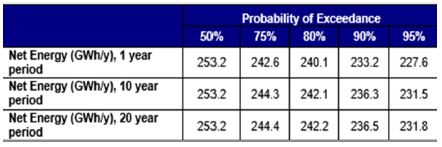

PB Power used an industry standard modeling tool (WAsP), in conjunction with proprietary software developed in-house to calculate the energy production. PB Power’s proprietary tools have been designed and verified based on their Quality Management procedures and guidelines. From the computational wind flow modeling of the GAWIP, the net average annual energy output produced by the wind farm’s 49 WTGs was predicted to be 253 GWh, for 96% availability.

Probability of exceedance

A statistical uncertainty analysis was carried out to study the parameters contributing to the variability and uncertainty of the results. The net energy yield for certainty levels of 50%, 75%, 80%, 90%, and 95%, are given in the table for one year, ten year and 20 year periods as shown below.

Probability of exceedance

3.3 Wind farm and turbine generator

The wind farm consists of three main components:

● Wind turbines, 49 WTGs;

● Balance of plant, consisting of the internal electrical reticulation systems, roads, hard stands, and foundations;

● Grid connection consisting of an on-site 22.9/154 kV substations, approximately 7 km of 154 kV overhead transmission and 2.7 km 154 kV underground cable.

Site map

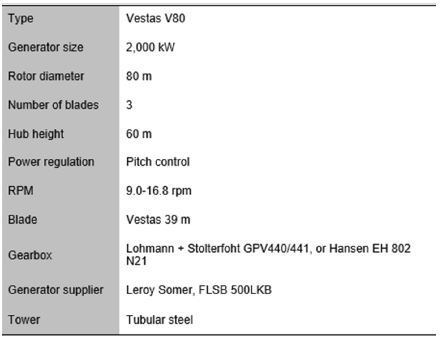

The Project installed 49 units of V80-2.0 MW wind turbine generators (WTGs) with state-of-the-art pitch regulation control technology to be provided by Vestas, the world leader in WTGs with over 35% of the global market. At that time, more than 1,145 units of this turbine type were installed worldwide. Vestas updated V80 with relevant improvements based on its experience, and it should be considered proven technology, provided that it has been sold since 2001.

Specification of WTG

49 wind turbine generators were lined up with a relatively low spacing of three rotor diameters, along with the two ridges, transversal to the main wind direction. This layout is assessed to be the most favorable about total energy production, wind farm efficiency and minimum turbulence loads on the equipment. The availabilities of typical V80 units well-met industry standard above 96%. The EPC contract also guaranteed a level of 96% availability. The EPC contract specifies a warranted power curve for various operating conditions i.e. Power Curve Performance LDs effectively compensate GAWIP for lost revenues for each percentage of power curve below 95% that is not achieved and similarly for the availability below 96% in the five years of the warranty period.

This warranted power curve is based on the site’s typical air density and is in line with measurements for V80-2 MW turbine type carried out by credible international measurement institutes. PB Power was of the opinion that the availability level warranted for this turbine type is reasonable and achievable.

3.4 Regulatory Framework

In 1987, the “Alternative Energy Development Promotion Act” was enacted to establish a regulatory basis for the promotion of renewable energy in Korea. The FIT system was introduced in 2002 to support renewable energy generation cost.

In these regulatory frameworks, electricity produced by the wind power generators are sold to KPX on a priority basis based on a price of KRW 107.66 /kWh for 15 years (Standard Price). This policy allows the Project to mitigate the risk of price fluctuation, one of the major variables that may cause revenue instability. This tariff structure was applicable for 15 years post initial completion, on the condition that the accumulated capacity of the wind producers is within 250 MW and is commissioned prior to 11 October 2006. This tariff support together with the subsidized funding via the KEMCO loan program was also in line with the governmental policy of promoting renewable energy and expanding the portion of generation in Korea from its 2.3% in 2005 to 5% by 2011.

3.5 Funding

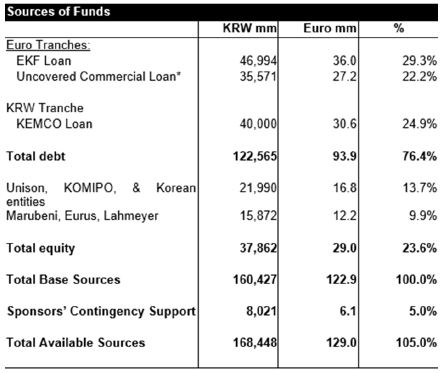

The Project was funded through a combination of equity and limited-recourse Project Finance debt. KRW37,862 million was funded by equity, representing 23.6% of the Project Cost. The equity was funded upfront (i.e., before drawdown of any debt) to save some interest during construction from the Sponsors’ perspective and to mitigate the equity funding risk from the lenders’ perspective. The debt, representing 76.4% of the project cost consisted of (1) an EKF supported EUR36 million 10-year amortizing loan fully guaranteed by EKF, the Danish ECA; (2) an EUR27.7 million uncovered commercial 11.5-year amortizing loan; and (3) a KRW40 billion 15-year amortizing KEMCO loan. The Project financing structure for the project cost is summarized below:

Sources of funds

At the financial closing, the GAWIP was required to lock into hedging arrangements for both construction and operation phases i.e. interest rate swap for 100% of the uncovered commercial loan from Euro floating interest rate to Euro fixed interest rate for the construction phase. No such requirement was asked for the EKF loan, and KEMCO loan as a fixed rate of CIRR7) applies to EKF loan and the project benefits from a low and stable interest rate for KEMCO loan. For the operation phase, it was required to enter into cross-currency, and interest rate swaps for all Euro denominated loans to have a fixed KRW interest rate and a fixed KRW principal repayment profile to hedge the KRW denominated revenue stream. Again, no such requirement was needed for KEMCO loan due to natural currency hedging and a low and stable interest rate provided by KEMCO.

All the three tranches of the debt were ranked pari passu together with swap payments in respect of security and lender rights. The principal repayment profile was sculpted and achieved an average debt service cover ratio of 1.83x in the P75 case (the base case, which itself is a conservative case as compared to P50) and a minimum debt service coverage ratio of 1.39x. The ratios gave lenders a fairly high degree of comfort, compared with other similar power projects.

4. Results and analysis

Based on the facts and data obtained from the GAWIP, we will review individual factors and see how well the GAWIP has implemented for the four key success factors discussed earlier.

4.1 Feasibility Analysis (B1)

For an in-depth analysis of the feasibility, the previous study suggested five criteria: plural independent technical consulting firms for the survey, economies of scale, easy connection to the grid, infrastructure for construction and, lastly, site location remote from a residential area.

In Gangwon case, it has an ideal location with proven wind resource so that the above criteria are well met. LI, on the sponsor side, and PB Power, on the lender side, conducted separately the wind resource survey using the dataset accumulated from four monitoring sites on top of existing dataset of relevant authorities and the surveys produced reliable results. Meanwhile, all other infrastructure was properly arranged for grid connection, construction, transportation of materials, fairly remote from the residential area, including but not limited to the benefits of economy of scale. In fact, GAWIP is still the biggest wind farm commercially operating in Korea.

4.2 Wind Turbine Generator (E1)

Needless to say, wind turbine generator is a key device in wind power generation system. It has an organic relationship with other key success factors so needs to perform optimally in consideration of other elements including the convenience of service and parts procurement, the cost-efficiency of maintenance, and quick troubleshooting to minimize the idle period.

GAWIP deployed the technically proven wind turbines of Vestas, which ranks the top manufacture in the global wind turbine market. The availabilities of typical V80 units well meet industry standard above 96%. The EPC contract also provided a guarantee for a level of 96% availability.

The Figure below is a graph of the actual operating results over the last 12 years. The blue line is the monthly average wind speed, the gray line is the capacity factor, and the red line at the top of the graph indicates the availability of the WTG. It is seen that the seasonal effect is apparent and the capacity factor is very proportional to the wind speed. Availability of WTG went down temporarily as low as 85.3% at the start stage, but it recovered immediately and perform very stably during operation until now.

Wind performance

4.3 Government Tariff System (B3)

Due to the nature of the renewable energy generation, the cost of generating electricity is higher than that of conventional fossil fuels, so a variety of regulatory supports are needed to guarantee the profitability of the power generation. The FIT system, which compensates a certain portion of the gap between SMP and the standard price, has expired in 2011 and is now substituted with the RPS scheme.

Electricity sale price

GAWIP is guaranteed to secure a minimum price of 107.66 / KWh for 15 years for electricity sales. Moreover, if the SMP exceeds this Standard Price, the higher price is automatically adapted for the sale, so GAWIP benefits from the minimum standard price and more as highlighted in green in the graph. In recent unusual situation caused by low oil price, SMP remains below the Standard Price, even touching the level of KRW60/kWh but sales have been systematically guaranteed, contributing significantly to the stable profit structure of the company.

4.4 Project Finance (A5)

Renewable energy projects, including wind power generation, in general, require large-scale funding for the purchase of wind turbine generators and site construction. In most cases, external borrowing from the pool of financial institutions is common at the debt-to-equity ratio of 80:20 for the project cost. The higher the debt ratio, the higher return the borrowers can expect on their equity from the viewpoint of the leverage effect, but the greater the repayment obligation and risk. Therefore, it is important to calculate and set up the appropriate ratio according to the size of the project or the expected sales.

Once project finance is utilized, lenders are interested in reducing the risk of relatively low return on their lending and/or the non-payment risk. Thus the gearing level is limited by the lenders, while putting vigorous covenants to restrict the size and the use of the loan. For instance, Debt Service Coverage Ratio (DSCR), which indicates the ability to pay interest and installments in the cash flow of a project, is one of the most widely used financial covenants. The ratio can be simply calculated for the net cash flow to principal and interest obligations. A DSCR that is below 1 implies a negative cash flow. For instance, a DSCR of 0.90 indicates that the company’s cash flow available for the debt service is enough to cover only 90% of its annual debt payments. The DSCR is, therefore, a benchmark used to measure the cash generating ability of a project entity to cover its debt payments.

It was analyzed that GWAIP can support the envisaged debt as demonstrated by an average debt service coverage ratio (DSCR) of 1.83x (min 1.39x) on a conservative P75 basis, being the Base Case. On the P90 basis, the average and the minimum DSCRs are 1.77x and 1.33x, respectively.

DSCR trend

Looking at the DSCR trend over the past ten years, GAWIP demonstrated it was fully feasible to meet the debt service with the cash flows as originally scheduled, even though showing a temporary breach below the minimum DSCR in 2009 due to the shortage of electricity production. Overall, DSCR, an indicator of healthy financial status, has far exceeded the minimum level that was established. As of the end of 2016, it stands at 1.2, which implies that foreign-currency borrowings are to be repaid in full as of March of this year, and no need to further comply with the ratio, which indicates more dividends are available to shareholders. The fact that the DSCR covenant is in good compliance without problems means that the project has been operating according to the original cash flow projection.

Another noteworthy point is GAWIP was structured to well protect from financial risks such as interest rate and exchange rate. Of the borrowings, approximately 68%, which are Euro denominated, have a fixed rate through either a fixed rate of CIRR (in respect of EKF tranche) or an interest rate swap (in respect of Uncovered Commercial tranche) during the construction phase. All have a fixed KRW interest rate through a cross currency and interest rate swap during the operation phase. This creates no risk arising from interest rate change linked to these tranches. All hedging transactions were entered into as a conditions precedent to drawdown.

EURIBOR and FX rate

As can be seen from the above graph, fluctuation trend of the interest rate and the exchange rate over the past ten years show that the fluctuation is extremely large. In the case of the exchange rate, the fluctuation of the lowest point about the peak was more than 60%, and the interest rate has changed from the level of 5% to the recent negative rate. Without proper hedging, the project may be put in great danger.

5. Conclusion and Implications

In this paper, we intended to analyze the effectiveness of the success key factors of wind power projects referring to the previous study by applying them to the case of Gangwon wind power generation which is being operated with successful results.

Among the various factors, “Feasibility analysis,” “Government tariff system” and “WTG selection,” and “Project Finance” are selected to be the key factors for the success. When they fall below a certain level, they will hamper investors' profitability and may drive the project into a catastrophic situation in some cases. In particular, Project Finance, as opposed to the three other factors determined or assumed at the project planning stage, would seriously affect the profitability of the project throughout its operating period due to its nature of volatility. For example, daily fluctuations of interest rates and exchange rates would significantly affect the debt serviceability for foreign currency borrowings and trigger the default in the worst situation. It is, therefore, necessary to arrange adequate countermeasures against such fluctuations at the project modeling stage and carefully manage them during the operation period.

In this paper, we can see how these key risks and success factors were analyzed and effectively managed in the case of Gangwon Wind Power, which is proven to be profitable and successful for the past ten years. As for the financial risk related to project financing, the core factor of success, several measures can be suggested to mitigate the foreign exchange risk. First, localization of WTGs and encouragement to use for domestic wind farms would fundamentally exclude engagement of foreign currency loan and the relevant risk. However, this assumes the technical reliability of domestic WTGs and the manufacturer’s capability of warranty. Second, it is needed to expedite development of various financial derivatives in the market so as to provide appropriate hedging products to cover the financial risks.

Limitations of this paper show that it would not be feasible to quantify the degree of interrelations between the four key success factors nor to draw quantitative measurements of the analysis results. And, Gangwon wind power, which is used for a case study, has operated under the FIT system and it is still receiving benefits from the mechanism of standard price, while all renewable energy projects are put under the RPS system since its launching in 2012, being applied with REC (Renewable Energy Certificate). Therefore, the key success factors under the new system are subject to revaluation in the context of new market conditions and business environments. In order to support and encourage development of renewable energy projects, it is of significance to study in depth and measure the appropriateness of REC price in association with the key success factors.

subscript

| WTG : | wind turbine generator |

| FIT : | Feed-In-Tariff |

| RPS : | Renewable Portfolio System |

| SMP : | System Marginal Price |

| PF : | Project Finance |

| GAWIP : | Gangwon Wind Project |

| DSCR : | Debt Service Coverage Ratio |

Notes

References

- Ali, B., Sopian, K., Chan, H. Y., Mat, S., & Zaharim, A., (2008), “Key success factors in implementing renewable energy programme in Malaysia”, WSEAS Transactions on Environment and Development, 4(12), p1141-1150.

- Blanco, M. I., (2009), “The economics of wind energy”, Renewable and Sustainable Energy Reviews, 13(6-7), p1372-1382.

- Chatterjee, S. K., (2013), “Promotion of Wind and Solar Energy through Renewable Energy Certificate System: Lessons from Renewable Obligation Certificate, United Kingdom experience for India”, http://siteresources.worldbank.org/FINANCIALSECTOR/Resources/000_India_Wind_and_Solar_Industry_9_10_2013.pdf.

- Deloitte, (2014), “Establishing the investment case Wind power”, Deloitte Touche Tohmatsu Limited.

- GWEC, (2017), Global Statistics, http://www.gwec.net/global-figures/graphs/.

- Kim, Y.K., & Chang, B.M., (2011), “풍력발전사업 프로젝트 파이낸싱에 불확도 [Uncertainties]가 미치는 영향 및 AHP를 이용한 개선방안 연구”, Korean Science Management Review Conference, p869-881.

-

Goh, H. H., Lee, S. W., Chua, Q. S., Goh, K. C., Kok, B. C., & Teo, K. T. K., (2014), “Renewable energy project: Project management, challenges and risk”, Renewable and Sustainable Energy Reviews, 38, p917-932.

[https://doi.org/10.1016/j.rser.2014.07.078]

- Kim, E., (2006), “풍력발전의 보급확대 전략: A National Strategy for Wind Power Dissemination”, New & Renewable Energy, 2(4), p93-101.

- Kim, H., Ko, K., & Huh, J., (2015), “Risk Factor Analysis in Wind Farm Feasibility Assessments Using the Measure-Correlate-Predict Method”, International Journal of Renewable Energy Research, 5(1), p230-235.

- Kim, Y., & Chang, B., (2013), ”풍력발전사업 에너지생산량 산정 오차가 사업성지표에 미치는 영향 및 AHP 를 이용한 중요인자 분석”, Korean Science Management Review, 30(2), p1-10.

- Lee, J. C., (2015), “RPS제도가 PF방식 LNG복합발전프로젝트의 사업성에 미치는 영향: Impact of Renewable Portfolio Standard System on the Feasibility of LNG Combined-cycle Power Projects based on Project Finance”, New & Renewable Energy, 11(1), p27-35.

- Lee, J., Park, M., Lee, Y., & Kim, J., (2007), “풍력자원의 불확실성을 고려한 사업자측면에서의 투자타당성: A Stochastic Analysis of a Wind Power Investment”, New & Renewable Energy Conference, p357-360.

-

Lyou, A.S., Kim, B.G., & Kim, H.K., (2012), “풍력 발전소 프로젝트의 핵심성공요인: Critical Success Factors for Wind Power Projects”, Korean Journal of Construction Engineering and Management, 13(1), p140-147.

[https://doi.org/10.6106/kjcem.2012.13.1.140]

- Park, K., Jung, J., Lee, M., & Kim, D.H., (2006), “강원풍력발전 CDM 사업 사례 연구: Study on Gangwon Wind Park CDM”, New & Renewable Energy Conference, p298-303.

- Ryu, S., Um, S., & Kim, S., (2009), “풍력발전이 SMP에 미치는 영향: An Analysis of the Impact of Wind Power Generation on SMP”, New & Renewable Energy Conference, p208-211.

- Scalone, C., (2009), “Key success factors for the development of wind energy”, edp renovaveis.

-

Sundaresan, S., & Wang, N., (2007), “Investment under uncertainty with strategic debt service”, American Economic Review, 97(2), p256-261.

[https://doi.org/10.1257/aer.97.2.256]

- Toke, D., S. Bruekers, M. Wolsink, (2008), “Wind power deployment outcomes: How can we account for differences?”, Renewable and Sustainable Energy Reviews, 12, p1129-1147.

- 한국전기연구, (2012), RPS 정책방향 및 REC 거래시장.

- 신재생에너지공급의무화제도 및 연료혼합의무화제도 관리운영지침 (산업통상자원부 고시 제2015-155호) (1).